Africa Tech Insights

Insights into Africa's Tech Evolution

Analysis

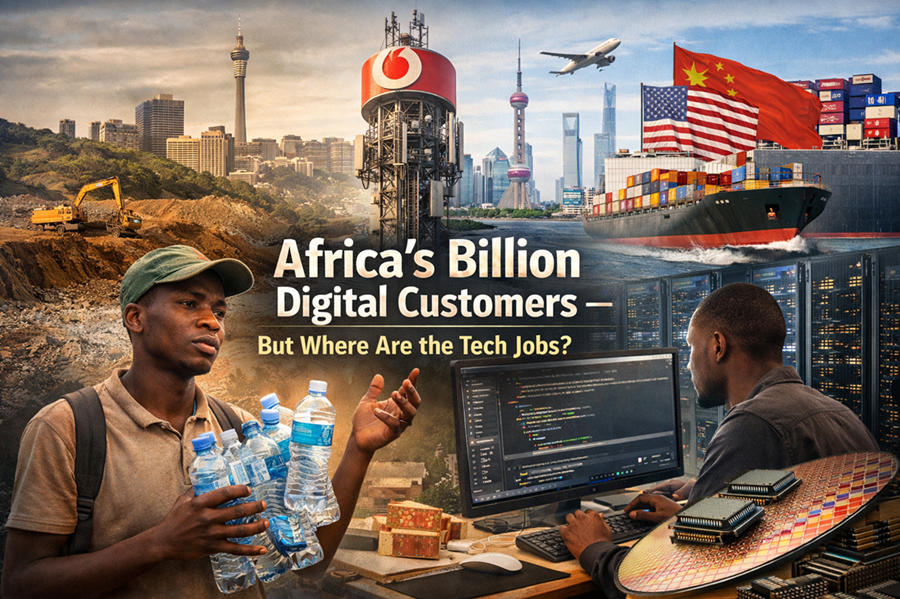

Africa’s Billion Digital Customers — But Where Are the Tech Jobs?

Africa has become one of the fastest-growing digital markets in the world, with hundreds of millions of mobile and internet users powering global technology platforms. Yet despite this enormous consumer base, the continent captures only a small share of the high-value technology jobs behind those platforms.

By Ahmed I Elmi |

Estimated Reading Time: 7 min |

Total Words:

1318 |

Published: 15 March 2026

| 92 views

By Ahmed I Elmi |

Estimated Reading Time: 7 min |

Total Words:

1318 |

Published: 15 March 2026

| 92 views

Image Credit: Image generated using AI for illustrative purposes.

In Context

Over the past two decades, Africa’s digital transformation has accelerated rapidly. Mobile networks have expanded across the continent, bringing internet connectivity to areas that once had limited infrastructure. Fintech services have enabled millions of people to access digital payments, banking, and e-commerce for the first time.

Telecommunications companies such as Vodacom, linked to the global operations of Vodafone Group, as well as MTN Group, Airtel Africa, Orange S.A., Etisalat, and Telefónica serve tens of millions of customers across African markets. In parallel, global technology firms such as Google, Microsoft, Amazon Web Services, and Meta Platforms provide cloud infrastructure, data services, and digital platforms that underpin much of Africa’s online economy. These companies are central to the continent’s digital infrastructure, yet a significant share of high-value technical work—such as cloud architecture, advanced software engineering, and AI development—remains concentrated outside the continent.

African markets often host the customers, while advanced technology jobs—cloud architecture, telecom software engineering, cybersecurity design, and artificial intelligence development—are located in technology hubs such as Seattle, Silicon Valley, London, or Berlin.

Africa has more than two thousand universities, yet only a limited number focus heavily on advanced telecommunications research or large-scale software infrastructure. As a result, many graduates enter the labor market with technical skills but face limited opportunities to apply them locally.

Source: CBRE Global Tech Talent Guidebook 2025.

Source: CBRE Global Tech Talent Guidebook 2025.

Zoom In: The Telecom Case Study

The structure of telecommunications companies operating in Africa offers a clear example of this imbalance. Vodacom serves more than 130 million customers across African markets. Yet in some countries, the local workforce remains relatively small compared with the scale of the customer base. For example, Vodacom Tanzania employs roughly several hundred staff members while serving millions of subscribers.

Local offices primarily manage:

-

sales and marketing

-

retail operations

-

customer support

-

regulatory compliance

However, the most advanced technical functions—such as network architecture design, large-scale software systems, and cloud infrastructure development—are frequently managed in global technical centers connected to Vodafone Group. This pattern is not unique to telecommunications. Similar dynamics exist across cloud computing, digital platforms, and many global technology companies. Millions of African customers generate revenue through subscriptions, data usage, and digital services. Yet a significant portion of the engineering jobs linked to these services is located elsewhere.

The Graduates With Nowhere to Go

The consequences of this imbalance are visible across many African cities. Every year, universities produce graduates with degrees in computer science, information technology, and software engineering. These young professionals study programming languages, network architecture, and data systems in hopes of participating in the global digital economy. Yet in some cases the local job market cannot absorb them. It is not uncommon to encounter computer science graduates working outside their field—sometimes selling small goods such as bottled water, phone accessories, or other products in informal markets simply to earn a living.

This situation does not reflect a lack of talent or ambition. Rather, it reflects the structural reality of a digital economy where many platforms are built, maintained, and controlled from overseas technology hubs. A cloud service used by an African startup may be hosted on servers managed by engineers in North America or Europe. The African company pays for the service, but the engineering jobs tied to that infrastructure remain abroad.

Zoom Out: The China Comparison

The contrast becomes clearer when compared with the strategy adopted by China during its rise as a technology powerhouse. China did not simply become a large consumer market for foreign technology companies. Instead, it used its enormous market size as leverage.

Foreign companies that wanted access to the Chinese market often had to:

-

establish local operations

-

form joint ventures with domestic firms

-

transfer certain technological capabilities

-

employ and train local engineers

This approach helped China build a domestic technology ecosystem that eventually produced global companies such as Huawei and ZTE. Today these firms employ tens of thousands of engineers and operate major research laboratories around the world. China’s strategy demonstrates how a large consumer market can be used as bargaining power to generate local technology employment and industrial capability. Africa, by contrast, has often opened its markets without negotiating similar employment or technology development commitments.

The Colonial Paradox

This pattern has historical echoes. During the colonial era, European powers extracted raw materials from Africa—minerals, agricultural products, and other resources. These materials were shipped to Europe, where they were processed and manufactured into finished goods. The manufacturing process created employment and industrial growth in European economies. The finished goods were then sold back to African markets.

In simple terms, this how goes:

-

Africa provided raw materials

-

Europe created industrial jobs

-

Africa became a consumer market

In some ways, the digital economy risks repeating a similar structure. Instead of raw materials, Africa now provides digital consumers and data usage. Instead of factories, technology infrastructure and engineering jobs are located in advanced economies. The result is a modern version of an old economic pattern: value creation happens elsewhere while consumption happens locally.

Source: International Telecommunication Union – Global ICT statistics

The Trade War Connection

This dynamic also helps explain global debates about trade and economic policy. When Donald Trump launched a series of tariffs on imports from China during the US–China trade war, the argument was partly about protecting domestic employment. Supporters of the tariffs argued that decades of globalization had allowed manufacturing jobs to move overseas while American consumers benefited from cheaper imports. The policy response was an attempt to rebalance that relationship by encouraging production and employment to return domestically. Whether one agrees with that strategy or not, the underlying concern is similar: who captures the jobs in a globalized economy?

Africa faces a comparable question in the digital age. If African markets generate large revenues for global technology companies, should those markets also capture a greater share of the jobs connected to that economic activity?

When “Open Markets” Are Not Enough

Globalization is often described in terms of open markets and free trade. But an open global economy does not automatically guarantee balanced outcomes. If one region primarily supplies consumers while another region captures the high-value jobs, innovation capacity, and intellectual property, the benefits of globalization may become unevenly distributed.

This is why many countries pursue industrial policies designed to strengthen domestic capabilities in strategic sectors such as:

-

semiconductors

-

artificial intelligence

-

telecommunications

-

cloud computing

These policies aim to ensure that economic participation includes not only consumption but also production and innovation.

The Strategic Question for Africa

Africa’s digital economy is still developing, and the continent holds enormous potential. With the world’s youngest population and rapidly expanding internet connectivity, Africa could become one of the most important technology markets of the 21st century. But the long-term outcome will depend on how African countries position themselves within the global digital system.

Key questions include:

-

Should African governments encourage technology companies to build local engineering hubs?

-

Should universities expand advanced computing and AI programs?

-

Should digital infrastructure projects prioritize local talent development?

-

Should large technology firms be encouraged to employ more engineers within the markets they serve?

These decisions will shape whether Africa becomes primarily a consumer of global technology or a producer of technological innovation.

The Opportunity Ahead

The current imbalance is not inevitable. History shows that countries can transform their economic roles through deliberate policy choices, education investment, and strategic negotiation with global industries. Africa’s growing digital market provides leverage. Hundreds of millions of users rely on mobile networks, cloud platforms, and digital services every day. If that market power is used effectively, it could help create more local opportunities for the next generation of African engineers and innovators.

For now, however, the paradox remains clear: Africa has millions of digital customers—and thousands of talented technology graduates—yet many of the highest-value technology jobs connected to those platforms still lie far beyond the continent’s borders.

This is an opinion piece. The views expressed in this article are those of just the author.